The Quest for Retirement Assets: When the Light Shines on the Fiduciary Standard

Abstract

In response to the Department of Labor (DoL) Rule, some of the wirehouses and larger independent broker-dealers (IBDs) have decided to take drastic steps.

Celent has released a new report titled The Quest for Retirement Assets: When the Light Shines on the Fiduciary Standard. The report was written by Kelley Byrnes, an Analyst with Celent's Securities & Investments practice.

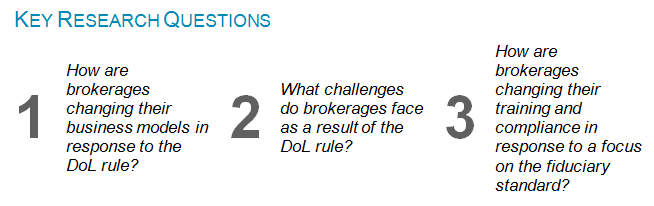

This report explores how brokerages are changing their fee structure, as well as training and compliance, in response to the industry focus on the fiduciary standard.

In response to the Department of Labor (DoL) Rule, some of the wirehouses and larger independent broker-dealers (IBDs) have decided to take drastic steps. Merrill Lynch has decided to ban commissions in retirement accounts. Other firms have decided to employ the Best Interest Contract Exemption (BICE) to allow advisors to receive commissions if their clients sign an agreement first.

Regardless of whether firms decide to ban or keep commissions, firms are changing their business model from a product-centric to an advice-centric model. Additionally, enterprises and advisors must come up with a clear explanation of their services, reinforcing that they are working in the best interest of their clients. Investors are becoming increasingly aware of the “fiduciary” standard.

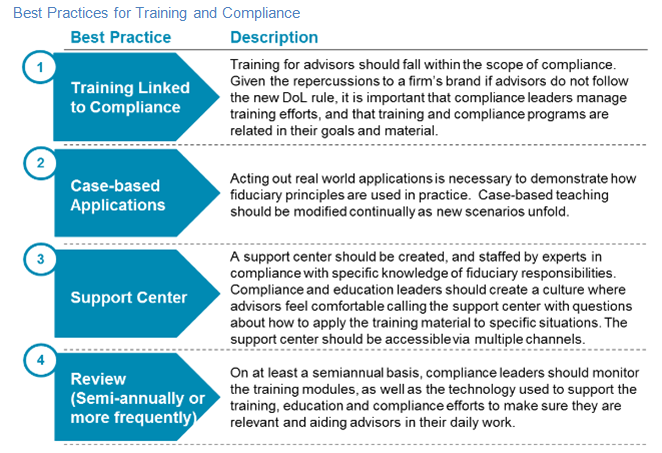

Banks and brokerages are providing fiduciary and retirement-specific training to advisors, and in turn, creating designations for advisors who satisfy the requirements. Firms are hiring specifically for retirement specialist roles, where individuals interact with retirement plan participants and sponsors.

“The specific titles and credentials that brokerages bestow on advisors can be misleading to investors. It would be helpful if an independent third party created a meaningful test that could be applied across wealth management firms. fi360 is one of the companies working toward this goal,” commented Byrnes.

“Over the next 12 to 18 months, it is certain that more vendors will create solutions to aid firms and advisors in their efforts to provide fiduciary training and comply with the DoL rule,” she added.