The Banking Crisis: A Back to Basics Lesson

Abstract

Many of the top banks in the US are in deep trouble, and some no longer exist. Is the entire financial system at risk?

In a new report, The Banking Crisis: A Back to Basics Lesson,Celent explains the origins and implications of the banking crisis.

The crisis has not impacted all banks equally. Large banks have suffered much more than smaller ones. While they have an advantage in efficiency, they have demonstrated that, as a group, they take on greater risk and are not sufficiently compensated for doing so.

Large banks have forgotten a simple tenet of the banking industry, the three C’s of credit:

1. Capacity (to pay) 2. Character (or credit history) 3. Collateral

Banks that were originating loans for securitization generally looked only at collateral and expected real estate prices to rise forever, ignoring the first two C’s. Low documentation loans (aka "liar’s loans") were an accepted part of the landscape.

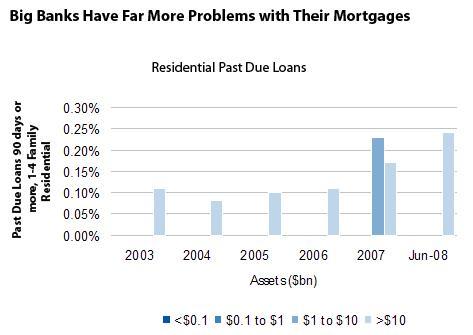

In the above chart, banks are broken into buckets by asset size, the largest bucket being banks with over $10 billion in assets. An examination of these charts shows a consistent pattern of the largest banks being the least effective in understanding the risk in their portfolios.

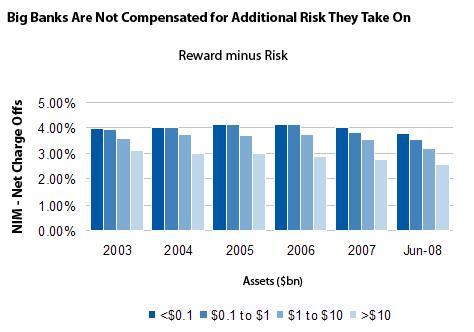

One broad way of measuring reward to risk is net interest margin (reward) less net charge-offs (risk). As shown below, the largest banks have the poorest results during good times and bad.

"Large banks tend to look at mortgages as something to be originated and sold. They forgot about the risks associated with originating and warehousing loans," says Bart Narter, senior vice president of Celent’s banking group and author of the report. "There are large banks that have weathered the storm and become the acquirers. Poorly run banks are now under new ownership."

Small banks also have an efficiency disadvantage that forces them to have higher costs. In order to survive, they must generate higher revenue, taking on loans the larger banks have chosen not to fund, but receiving compensation for their efforts.

The 30-page report contains 23 figures. A table of contents is available online.

of Celent's Retail and Business Banking and Corporate Banking research services can download the report electronically by clicking on the icon to the left. Non-members should contact info@celent.com for more information.