Mobile B2X: The Next Mobile Payment Wave in International Markets

Abstract

The developing world has seen the greatest adoption of mobile payments. It is now on the verge of a whole new payment segment: “mobile B2X,” or businesses’ use of the mobile channel to pay other companies, employees, and residents.

In many countries around the world, mobile person-to-person payments have become the success story of the mobile payments arena. They have grown so popular that they are being offered by mobile network operators (MNOs) in dozens of countries across Africa, Asia, and Latin America. It is only a matter of time before increased competition leads to service commoditization and price compression.

Players in the mobile payments space will have to start looking for new markets and areas of innovation. In this report, Mobile B2X: The Next Mobile Payment Wave in Developing Markets, Celent examines how companies and other institutions are beginning to use mobile payments for a number of important use cases:

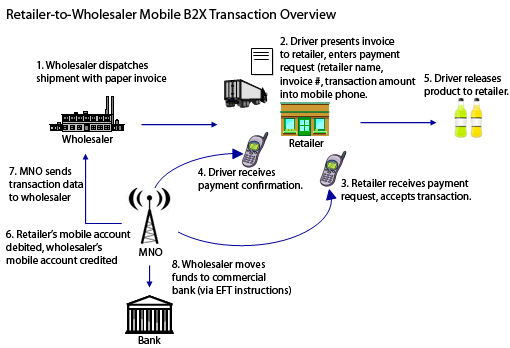

- Payments made by retailers to wholesalers for receipt of consumer goods.

- Salary, commission, and pension disbursements made by companies (and governments) to individuals.

- Social benefit distributions from companies (and governments) to individuals.

In countries where the majority of the population is unbanked, mobile B2X can occupy the role held by direct deposits in industrialized countries. Given that 1.7 billion of the world’s unbanked population will have a mobile phone by 2012, and using the Kenyan minimum wage as a proxy, the salary target disbursement “universe” is an astounding US$16.5 trillion.

"Mobile B2X is significant in that will finally provide a place at the mobile payments table for banks, given that banked entities (i.e., businesses and governments) will be market participants,” says Red Gillen, senior analyst with Celent’s Banking Group and author of the report. “Mobile B2X not only represents new revenue streams for banks. It also presents an opportunity to break the MNOs’ stranglehold on the mobile payments ecosystem."

However, mobile B2X market growth will not come easy, and technology alone will not be the “magic bullet” for success. Mobile carriers’ agent networks will need to be strengthened to play a greater cash-in/cash-out role. Government regulation will have to be monitored to prevent transaction limits from being too low. Current business models based on discrete functionality will have to give way to interoperability between mobile networks, banks, payers and payees. This will create an opportunity for technology vendors that can offer one-stop integration for payers and payees alike.