The New Liquidity Risk Management Paradigm: Restructuring Foundations for Best Practices

Abstract

Liquidity risk has been at the epicenter of the evolving subprime crisis, and management of this previously underappreciated risk has suddenly moved to the top of executive, practitioner, and regulatory agendas.

The subprime mortgage-induced market turmoil that started in the third quarter of 2007 is predicted to be one of the more severe crises in recent history in terms of duration, depth, and cost to financial institutions, as well as the broad global economy. The main lesson to be learned from this crisis is the need to return to the fundamentals so that liquidity risk management practices can be updated in accord with the paradigm shift in financial intermediation. Although many institutions’ balance sheets have shifted away from the basic premise of "deposits funding loans," liquidity risk management practices have not evolved in tandem.

In a new report, , Celent discusses the "risk du jour" in a comprehensive way, including common approaches and pitfalls, best practices, and next steps within the context of the recent market turmoil. Celent asserts that recognizing the new realities and building appropriate risk management practices will ensure convergence to new market standards in the coming years.

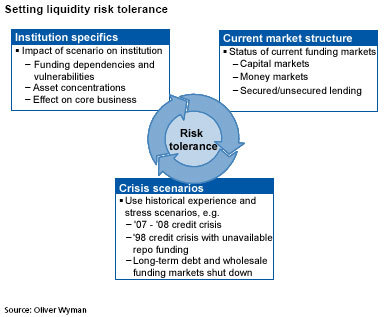

"Management of liquidity risk presents unique challenges and prudent practices need to recognize certain fundamental principles," says Umit Kaya, co-author of the report. "A major drawback in prevailing practices is disregarding the market and institution specifics in setting the level of risk tolerance. This senior-level issue will increasingly attract more attention. Similarly, institutions will have to overhaul their stress testing and scenario analysis frameworks, which also feed into the risk tolerance."

The report draws upon experience and observations from client work as well as other market reported events, both before and after the market turmoil began, in order to explore a number of key questions such as:

- What is the appropriate risk management response and what has the prevailing response been?

- What is the optimal framework to manage liquidity risk?

- How should the board and senior management be involved in liquidity risk management?

- What are the most pressing issues in the measurement of liquidity risk, especially in stress testing?

- How should institutions attempt to assess existing capabilities and analyze vulnerabilities in their current practices?

As such, it should be of interest to many stakeholders, including executives in search of tangible next steps, liquidity risk practitioners interested in the many dimensions of new challenges, and market participants in need of updating their understanding of financial institutions' liquidity exposures.

As a whole, the winners will be the institutions that can move quickly to build up their defenses and signal to the market that they have a robust framework in place that keeps their risks under control.

The 58-page report contains 21 figures and 8 tables. A table of contents is available online.

Members of Celent's Finance, Risk & Compliance research service can download the report electronically by clicking on the icon to the left. Non-members should contact info@celent.com for more information.